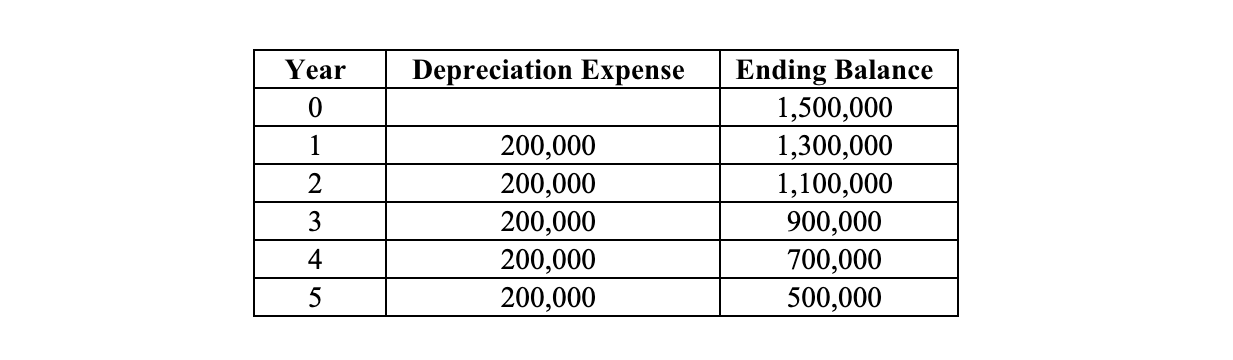

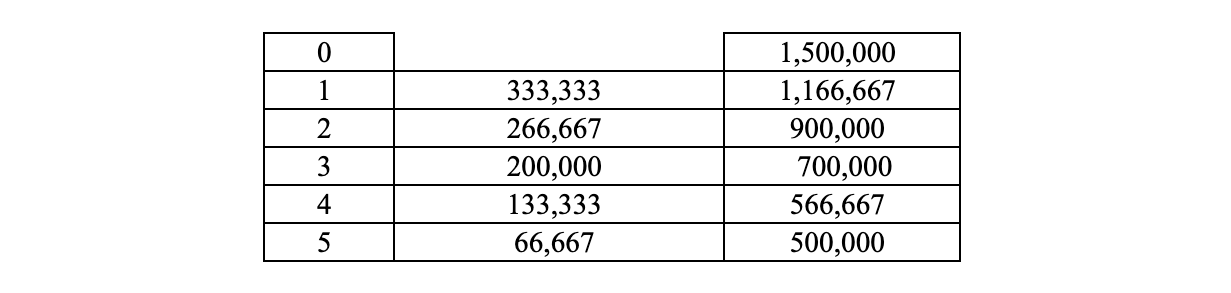

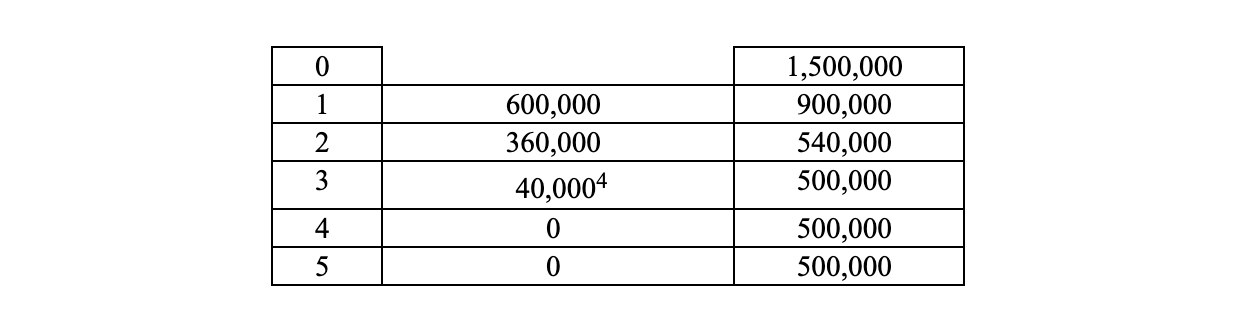

3.16: Resumen comparativo de los métodos de depreciación

- Page ID

- 69015

Dado:

Línea recta :

D epreciation acelerada Métodos :

- Suma de la- Y orejas 'Dígitos :

- Saldo doble/decreciente :

Nuevamente, D/DB es el más acelerado de los diversos métodos. El estudiante de finanzas necesita tener algún sentido de las “distorsiones” que los datos contables le presentan como resultado de la “elección” (de la gerencia y de los contables), y su impacto en análisis financiero. Además del método alternativo de depreciación s presente en este ejemplo, también podemos señalar que el valor de salvamento es una estimación n. Estas elecciones y estimaciones arbitrarias presentan “miradas” alternativas para los estados financieros, y dificultades interpretativas para el analista .

Nota Final : Los thre e m e thods cubiertos en las últimas páginas NO son aceptables para r Impuesto A ccounting. Ahí, un sistema totalmente diferente debe implementarse a raíz de una ley de 1986. El sistema tributario se llama “Sistema de Recuperación de Costos Acelerados Modificados”, o simplemente “MACRS”. Este método no se cubrirá aquí.